THX.V $

THX.L

Thor Explorations Announces Robust Results Of Independent Preliminary Feasibility Study And Maiden Probable Mineral Reserve At Segilola, Nigeria

September 27, 2017

Thor Explorations Ltd. (TSX VENTURE: THX) (“Thor” or the “Company”) is pleased to announce positive results for its Independent Preliminary Feasibility Study (“PFS”) and maiden Probable Mineral Reserve, prepared pursuant to National Instrument 43-101 (“NI 43-101”) for its 100% owned Segilola Gold Project (“Segilola” or the “Project”) in Nigeria.

The Project will be comprised of an open pit mine and will include the construction of a new 500,000 tonnes per annum (“tpa”) processing plant, which consists of a conventional crushing circuit, single stage grinding, carbon-in-leach, elution, electrowinning and smelting to produce gold dore. The PFS envisions a Project with a 17 month construction period and a 7 year mine life.

The Project description conforms with the Project’s existing 25 year Mining License “ML41” (renewed in September 2016) and approved Environmental Impact Assessment (“EIA”).

Preliminary Feasibility Study Highlights

All amounts stated in this news release are in US dollars (“$”) unless otherwise stated.

Base Case is stated at a gold price of $1,250.

NPV | Pre-tax NPV5% of $141m Post-tax NPV5% of $138m | Pre-tax NPV8% of $121m Post-tax NPV8% of $119m |

IRR | Pre-tax IRR of 53% with a 1.8 year payback on initial capital Post-tax IRR of 53% with a 1.8 year payback on initial capital | |

Capex | Pre-production capital of $71.4m | |

Production | Average of 81,000oz years 1-3 | Average of 47,000oz years 4-7 |

Production Cost | LOM C1 Cost of $613/oz LOM All-in sustaining cost of $682/oz | |

Mine Life | Current study mine life 7 years | |

Probable Mineral Reserves | 3.345Mt @ 4.2 g/t Au containing 448,000oz Au at 0.64 g/t cut off | |

Recoveries | Average metallurgical recoveries of 96% gold | |

Segun Lawson, President & CEO, commented:

“The Segilola Project benefits from many strong characteristics, including its high grade nature together with execellent metallurgy and attractive government fiscal incentives. This results in robust cashflows from commencement of operations and relatively low capital intensity. We are pleased with the results outlined in the Preliminary Feasibility Study which validates our belief in the potential of the Project. We believe scope exists to improve the Project economics as we continue to optimise and de-risk the Project through the Definitive Feasibility Study phase, which we aim to complete in H1 2018 and to then progress directly to Project development. The Project has significant exploration upside that can potentially both add to our open pit production and extend the life of mine as we continue to expore and assess the potential for a transition to underground mining operations.”

Economic Summary

The economic parameters quoted are based on 100% ownership of the Project and the fiscal incentive regimes (set out below) in place for the mining industry in Nigeria. The Project is 100% owned by Segilola Resources Operating Limited (“SROL”), which is a100% owned subsidiary of the Company.

The economic analysis excludes 26,600oz of Inferred Mineral Resources that is extracted in the PFS mine design and is treated as waste in accordance with NI 43-101 reporting guidelines. The PFS pit shell was selected to maximise economic mine life. In preparation for the Definitive Feasibility Study (“DFS”), the Company plans to undertake an infill drilling program, targeting the in-pit Inferred Resources, in addition to an extension drilling program. The Company considers that potential exists to upgrade and increase the existing Project Mineral Resource. The pit optimisation will be reviewed and mine design optimised during the DFS phase.

Table 1: Segilola PFS Project Economics

Gold Price ($/oz) | $1,050 | $1,150 | $1,250 | $1,350 | $1,450 |

Pre Tax | |||||

NPV5% ($m) | 69 | 105 | 141 | 178 | 214 |

NPV8% ($m) | 55 | 88 | 121 | 155 | 188 |

IRR (%) | 29% | 41% | 53% | 65% | 78% |

Payback (years) | 2.8 | 2.4 | 1.8 | 1.3 | 1.2 |

After Tax | |||||

NPV5% ($m) | 68 | 104 | 138 | 172 | 206 |

NPV8% ($m) | 54 | 87 | 119 | 150 | 181 |

IRR (%) | 29% | 41% | 53% | 65% | 77% |

Payback (years) | 2.8 | 2.4 | 1.8 | 1.3 | 1.2 |

Notes: Economics have been centered on a base case using a 8% discount rate and a gold price of $1,250/oz. Economics based on 100% equity financing with contractor mining. Payback period calculated on an undiscounted basis starting from production start. West African peers commonly use 5% NPV and these figures are quoted for comparison.

A summary of the capital costs, production and operating metrics from the PFS is provided below.

Table 2: Project Capital Costs | Table 3: LoM Project Operating Costs | ||||

Description | Cost ($,000) | Description | Cost ($/oz) | Cost ($/t) | |

Mining Capital(1) | 4,680 | Mining | 427 | 54.9 | |

Direct Plant Costs | 35,270 | Processing | 139 | 17.9 | |

EPCM | 10,130 | G&A | 42 | 5.5 | |

First Fills and Spares | 3,000 | Refining | 5 | 0.6 | |

Tailings and Water Storage Dams | 3,600 | Cash Operating Cost | 613 | 78.9 | |

Other Project Costs | 1,780 | Royalties(2) | 18 | 2.3 | |

Vehicles / Mobile Equipment | 850 | Total Cash Cost | 631 | 81.2 | |

Owners Costs | 5,610 | Sustaining Capital | 27 | 3.5 | |

Sub Total | 64,910 | Corporate G&A(3) | 24 | 3.1 | |

Contingency (at 10%) | 6,490 | All-In Sustaining Cost(4) | 682 | 87.7 | |

Total | 71,400 | ||||

LOM Sustaining Capital | 6,590 | ||||

Closure Costs | 5,000 | ||||

Notes: (1) Includes mining contractor mobilisation costs; (2) Vendor royalty – 3%, capped at $7.5m. Government royalty is assumed to be zero (refer to fiscal incentive regime below); (3) Corporate G&A allocated cost is quoted for AISC comparison and is not included in the Project economic analysis; (4) Quoted All-in Sustaining Costs are presented as defined by the World Gold Council and include Total Cash Costs, Corporate G&A, Sustaining Capital and Closure Costs.

Study Description

The Project focusses on the high grade gold deposit located 120km North East of Lagos. The deposit is located in Mining License number “ML41” which is surrounded by Exploration License “EL19066”. A paved road runs next to the Project affording ease of access.

The PFS is being compiled by Auralia Mining Consulting Pty Ltd. (“Auralia”). Auralia are responsible for the technical works relating to the Mineral Resource, Mineral Reserve including the mine design. In preparing the PFS, Auralia were able to draw on both detailed technical reports previously prepared for the Project and current work programs. Cost information from previous studies have been benchmarked against current costs and are considered to be within PFS confidence levels. Key contributors included AMTEC, who completed the metallurgical testwork, Sedgman, who carried out the process design and engineering and capital and operating cost estimates, Peter O’Bryan & Associates who carried out the geotechnical study, Peter Clifton & Associates, who carried out hydrology and hydrogeological studies and D E Cooper & Associates, who completed the design and cost estimates for the Tailings Storage Facility ("TSF") and Water Supply Dam.

A technical report in support of the Mineral Resource, the Mineral Reserve and PFS described herein and prepared in accordance with National Instrument 43-101 and Industry Guide 7 will be filed on SEDAR within 45 days of the Company’s updated resource announcement dated September 11, 2017.

Geology

The Project area is located in the crystalline basement complex rocks of southwestern Nigeria within the Upper Proterozoic rocks of the Ilesha schist belt which formed part of the Pan African mobile belt. At Segilola, gold mineralisation is localised within structural “compartments” defined by the intersection of two main controlling features: a westerly-dipping footwall calc-silicate suite of rocks and sub-vertical shear zones. Gold mineralisation is associated with stacked set of steep westerly-dipping, north-trending pegmatitic quartz-feldspar veins that intrude variably deformed gneissic rocks and schist. The vein system, which outcrops in places, extends over a strike length of about 2,000m and downdip to nearly 400m from surface. The gold itself is often coarse and visible in diamond core. There are opportunities to extend the known resource both along strike and down-dip.

Mineral Resource Estimate and Mineral Reserve

Mineral Resource Estimate

The PFS is based on an updated Mineral Resource model completed by Auralia. The Mineral Resource estimate was previously announced by the Company (refer to Company press release dated September 11, 2017).

Thor’s management believes that the Mineral Resources remain open to expansion and that there is an opportunity to improve the classification of the Inferred Mineral Resources with infill drilling. There is no certainty that such additional drilling will result in expanding or upgrading the classification of the Inferred Mineral Resources to Indicated category.

Table 4: Mineral Resource Statement, Segilola Gold Deposit as at September 11, 2017

Classification | Within Whittle Shell (Open Pit Resource) | External to Whittle Shell (Underground Resource) | Total | ||||||

(0.64g/tAu cut off) | (2.5g/tAu cut off) | ||||||||

Tonnes (Mt) | Grade (g/tAu) | Gold (oz) | Tonnes (Mt) | Grade (g/tAu) | Gold (oz) | Tonnes (Mt) | Grade (g/tAu) | Gold (oz) | |

Indicated | 3,926,000 | 4.3 | 539,000 | 111,000 | 4.7 | 17,000 | 4,037,000 | 4.3 | 556,000 |

Inferred | 835,000 | 5.1 | 137,000 | 1,195,000 | 4.4 | 169,000 | 2,030,000 | 4.7 | 306,000 |

Mineral Reserve

The Probable Mineral Reserve used in the PFS are the economically minable portions of the Indicated Mineral Resource as independently produced by Auralia.

Table 5: Mineral Reserve Statement, Segilola Gold Deposit as at September 27, 2017

Classification | Cut off (g/t AU) | Tonnes (Mt) | Grade (g/t Au) | Ounces Au |

Probable | 0.64 | 3,345,000 | 4.2 | 448,000 |

The Mineral Reserves are reported at an economic cut-off grade of 0.64g/t as determined by the following parameters.

Table 6: Mineral Reserve parameters

Parameter | Unit | |

Currency | $US | |

Base Mining Cost | $6.6 | $/bcm rock |

Mining Recovery | 95 | % |

Mining Dilution | 10 | % |

Background Dilution Grade | 0 | g/tAu |

Processing Cost | $21.9 | $/t ore |

Process Recovery | 96 | % |

Gold Sell Price | $1,250 | $/troy oz. |

Royalty(1) | 3 | % |

Discount Rate | 8 | % |

Mill Limit | 0.5 | Mill Mt/pa |

Notes: (1) Vendor royalty – 3%, capped at $7.5m.

Notes:

- For reporting purposes, based on the ‘reasonable prospects of economic extraction’ test, Mineral Resources are reported within an optimised pit shell, at a cut off grade of 0.64g/t gold, mining recovery of 95%, processing recovery of 96%, gold price of US$1,600/oz, processing costs of $21.9/t including on-site G&A and grade control. Mineral Resources with potential for economic extraction by underground mining methods, external to the optimised pit shell, are reported at a cut-off grade of 2.5 g/t gold. The Mineral Resource has been reported at the same cut off grade as the Mineral Reserve.

- The Mineral Reserve has been formulated as part of the PFS, and is based on open pit mine designs for which a mine production schedule and economic analysis have been conducted. The PFS assumes ore processing by standard CIL methods.

- The Mineral Resource and Mineral Reserve estimates have been prepared independently in accordance with the classification criteria of the National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101") and in accordance with the CIM Standards on Mineral Resources and Reserves, Definitions, and Guidelines prepared by the CIM Standing Committee on Reserve Definitions and adopted by the CIM Council.

- The Mineral Reserve estimate has been prepared by Anthony Keers (MAusIMM, CP Mining), the Mineral Resource estimate has been prepared by Chris Speedy (MAIG,#5349), both of Auralia Mining Consulting Pty Ltd, who are qualified persons under NI 43-101.

- Mineral Resources which are not Mineral Reserves do not have demonstrated economic viability.

- The Mineral Resource estimate is reported from an Ordinary Kriged block model.

- Unless otherwise noted, the Company's Mineral Resources are estimated using appropriate lithological interpretations, grade compositing and grade estimation techniques.

- The Company has adopted industry-standard procedures for sampling, data verification, compiling, interpreting and processing the data used to estimate Mineral Reserves and Mineral Resources.

- Mineral Resources are inclusive of Mineral Reserves.

- Numbers may not sum due to rounding.

- The Mineral Reserves are estimated using appropriate cut-off grades based on an assumed long term price of $1,250 per ounce of gold. Mineral Reserves are estimated using appropriate process recoveries, operating costs and mine plans that are unique to this project and include estimated allowances for dilution and mining recovery.

Figure 1: Final Mine Design

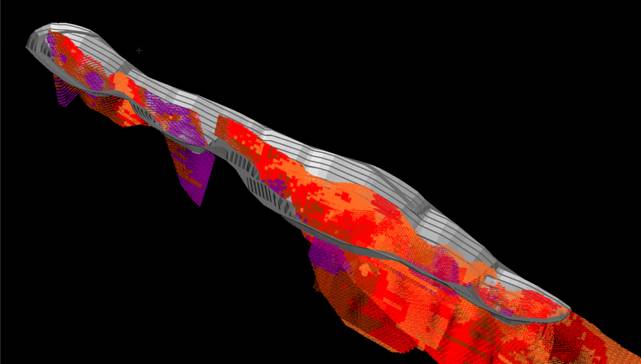

Mining Operations

The mine is to be developed in three stages, incorporating two interim stage pits. Mining operations will be carried out using conventional drill and blast and load and haul mining methods with 3.5Mt of ore and 62.0Mt of waste being extracted over a period of seven years

A detailed mining schedule has been developed that requires minimal pre-stripping prior to plant commissioning. Production will initially commence from the high grade northern pit, which outcrops at surface and along with the Stage 2 pit which commences after four months will return an average head grade of approximately 7.0g/t for the first 15 months of operation. Stage 3 commences in month 32 with a cut back of the southern wall of the Stage 2 pit to the final pit design.

The overall pit wall angles are based on recommendations from independent geotechnical consultants Peter O’Bryan & Associates. A further work program is planned for geotechnical, hydrological and general operational aspects such as dewatering studies and slope depressurisation. The results of these programs will be considered in the DFS.

The Company intends to engage an experienced mining contractor for the the drill, blast, load and haul operations. There are a number of well established regional and international mining contracting companies in West Africa. For the purposes of the PFS the Company obtained quotes from two contractors with relevant and current operating experience and benchmarked these quotes with other regional contractors.

Process Recovery

ROM ore will be delivered from the mine to the processing plant, which consists of a conventional crushing circuit and a single stage grinding circuit to achieve a target grind size P80 of 106 microns. The plant will operate on a 365 day/year, 24 hour/day operating cycle with a design plant availability of 91.3% for a nominal ore throughput of 62.5 tph resulting in a throughput rate of throughput rate of 500,000 tonnes per annum. Gold is to be extracted by conventional carbon in leach, to produce a gold dore via elution, electrowinning, and smelting.

Life of mine average gold recovery is estimated to be 96% resulting in life of mine production of 430,100 ounces from the currently stated Probable Reserves.

Services

Electrical power will be generated on site by the use of diesel powered generators. A total of three 1.6 MW generating sets will be installed and operated on a two duty, one standby basis.

The treatment of the ore will result in the production of approximately 500,000t of tailings per annum. The tailings will be pumped as a slurry to a tailings storage facility (“TSF”). The TSF will comprise single circular storage with an area of 24.6 ha. The TSF will be equipped with a centrally located decant tower which will enable water released from the tailings, and collected rainwater, to be returned to the plant for re-use. The TMF will be designed to International Standards.

Primary sources for process water at the Project will be decanted from the TSF and raw water make up the balance. Raw water will be supplied from a newly constructed water storage dam on a local creek. The water storage dam will be equipped with a spillway capable of allowing the excess water to be discharged to the river downstream of the dam. The spillway is likely to be in use for a large part of year as the run of river flow will exceed the plant requirements.

Environmental & Social

The Project has an existing EIA which has been approved by the Federal Ministry of Environment. The EIA approval is conditional on compilation of: (1) Environmental Management Plan (“EMP”); (2) Environmental and Protection and Restoration Plan (“EPRP”); and (3) Community Development Agreements (“CDAs”), which are required to be completed prior to operations commencing on site.

Both the EMP and CDAs are currently being developed and will be in place prior to the construction phase. The EPRP has recently been approved by the Ministry of Mines and Steel Development.

The Project does not require physical resettlement, however compensation for economic displacement and land acquisition for development activities is necessary. A Resettlement Action Plan is being developed to guide this process The Project provides considerable opportunity for improvement of socioeconomic conditions in the local area. Currently the local area and communities are underserved by social services and infrastructure and therefore the Project will look to enhance sustainable socio-economic development opportunities wherever possible.

To date the Project has maintained good relationships with local stakeholders and there is a common understanding of the Project development process. Community representation on the CDA committees has been established

A Project closure plan has been approved as part of the EPRP. Closure costs are estimated at $5m.

Fiscal Incentive Regime

Corporate Income Tax

Under the key incentive provisions of the Industrial Development (Income Tax Relief) Act (IDITRA”) and the Mining Act, the Project would benefit from a 5 year tax holiday followed by an accelerated capital allowance of 95% of mining expenditure. Following this period, the Project would be subject to standard Corporate Income tax of 30% on total profit.

Pioneer Status

The Mining Industry in Nigeria has been granted “Pioneer Status” which in accordance with the provisions of the IDITRA, provides for the grant of a tax holiday for a period of 3 years which may be extended at the end of the initial 3 years for a period of 1 year and thereafter for another period of 1 year or for one period of 2 years upon satisfactory compliance with certain conditions.

Other Key Incentives

Free transferability of currency, remittance of foreign capital and an exemption from import duties.

Minerals exported from Nigeria are zero rated based on the provisions of the VAT Act.

Royalty

Royalties are payable by companies engaged in mining activities in Nigeria. Royalties are calculated on an ad valorem basis. The applicable royalty rates range from 3%-5% depending on the type of mineral (Gold is 3%). The Minister may grant a concession to a mineral titleholder to defer payment of royalty on any mineral for a specific period, subject to the approval of the Federal Executive Council.

For the PFS, including the formulation of the Mineral Resources and Mineral Reserves it has been assumed that the project will qualify for a government royalty concession.

Other Taxes

Nigerian companies engaged in mining activities are liable to education tax at the rate of 2% of their assessable profit. The educational tax is not applicable during the Pioneer tax holiday.

An impost in terms of the Industrial Training Fund Levy has been included which has been levied at the rate of 1% of the amount of the annual pay roll levy

Additional opportunities and near term plans

The following opportunities were identified during the PFS phase as potential optimisations to be reviewed during the DFS process.

Opportunity | Comment |

Conversion of inferred resources into indicated and continuing to grow resource and reserve base | Following interpretation of results from the recent drilling program at Segilola, the Company considers that following an infill program and an additional targeted drilling program, potential exists to further enhance the Project resource in preparation for the DFS. In addition, the discovery of several high grade hanging wall lodes has highlighted the potential for both additional open pit resources and down-dip underground operations. |

Detailed metallurgical test work to optimize recoveries and flow sheet inputs for design and construction | The design philosophy applied in the PFS was for a low cost processing facility whilst maintaining high levels of reliability, operability and maintainability. Metallurgical testwork undertaken on the Project confirms that the Segilola ore is amenable to straightforward CIL processing with recoveries acieveable above 97% with a 48 hour leach. The Company intends to undertake a broader metallurgical drilling and testwork program in Q4/2017 to Q1/2018. This program is designed to provide further definition and confidence in respect to the variability of the ore across the deposit. The additional metallurgical testwork is focussed on optimising the existing process flowsheet, prior to finalising the DFS design parameters. Specific opportunities include: (i) reviewing the grind size – the Company considers that there may be operational benefits from a reduction in grind size from P80 106microns to P80 75microns; (ii) gravity recovery circuit (existing testwork indicates 36-84% gravity recovery is achieveable); (iii) pre leach thickening; and (iv) the use of air or oxygen as an oxidant. |

Detailed Topographical survey | An accurate site survey is required prior to detailed site planning. The Company intends to carry out a re-survey of the entire Project area using laser distance measuring technology (LIDAR) which can penetrate dense vegetation sufficiently to provide an accurate ground surface survey. This will also provide invaluable information for future exploration. |

Geotechnical study with results to feed into an optimized mine plan | Specific geotechnical drilling is considered appropriate to provide more data, particularly in relation to the west wall design, with a view to optimising the main pit design and reducing mining cost. |

Hydrogeological studies | The hydrogeology conditions require further study in order to finalise the design to DFS level. |

Review of overburden removal during pre-production period, to align with construction of RoM stockpile pad, Tailings Storage Facility starter embankment and water dam | In preparing the PFS, pre-stripping was minimised. This approach was considered reasonable due to the outcropping of the ore body in the northern starter pit. During the DFS phase, the Project implementation plan will be considered to optimise construction and pre-operation implementation. Identification of construction material for the Project will be undertaken with overburden material being tested for suitability. |

Process existing tailings prior to commissioning of mill | A small amount of mining was undertaken on the Project in the 1940-1950 period. A limited amount of tailings exist on site. During the next phase, the Company will assess the tailings and if practical will incorporate processing of the tailings through the CIL circuit prior to commissioning of the mill. |

EPCM vs EPC lump sum turnkey (“LSTK”) contract | In preparing the PFS it was assumed that the Project would be implemented on an EPCM basis. The proposed process plant design is straightforward and the Company considers that by adopting an alternative EPC LSTK approach for the main Project components, overall cost savings may be achieved as well as streamlining and de-risking implementation and providing price certainty. Discussions with potential EPC contractors have been positive and the Company will consider this and the overall Project contractual framework during the DFS phase. |

Contract vs Owner operator | In preparing the PFS, it was considered that the Project was too small to warrant owner operated equipment. The overall philosophy therefore is based on the use of mining contractors. Whilst the use of mining contractor remains the Company’s base case approach, during the DFS, the Company will review other opportunities. |

Fundraising

The Company intends to undertake a fundraising in Q4 2017. Following the fundraising, the Company will initiate the planned workstreams with the objective of completing the DFS in H1 2018.

The fundraising will also enable a wider drilling program to be undertaken on the Company’s Markosa Discovery on it’s Douta exploration permit in Senegal.

Notifications to Investors

About the Segilola Gold Project

The Segilola Gold Project is located in Osun State of southwestern Nigeria approximately 120km from Lagos. High grade gold mineralisation is developed within Upper Proterozoic gneissic and schist sequences that are oriented parallel to the boundary between the West African Craton and the Pan African province. At Segilola, gold mineralisation extends from surface to a depth of up to 300m down dip over a strike length of 2km. The project area is served by good infrastructure that includes a sealed road to the proposed development site.

The Segilola Gold Project is 100% owned by Thor. It is fully permitted, with the mining licence renewed in September 2016 for a period of 25 years.

Qualified Person

The above information has been prepared under the supervision of Alfred Gillman (Fellow AusIMM, CP), who is designated as a “qualified person” under National Instrument 43-101 and has reviewed and approves the content of this news release. He has also reviewed QA/QC, sampling, analytical and test data underlying the information.

The Independent Mineral Resource was completed by Mr Christopher Speedy (MAIG, #5349), who is designated as a “qualified person” under National Instrument 43-101 and has reviewed and approves the content of this news release. The independent Mineral Resource estimate was completed using data provided by Thor Explorations Ltd, no issues were found during the review of all supplied data.

The Independent Mineral Reserve was completed by Mr Anthony Keers (MAusIMM, CP Mining), who is designated as a “qualified person” under National Instrument 43-101 and has reviewed and approves the content of this news release. The independent Mineral Reserve estimate was completed using data provided by Thor Explorations Ltd, no issues were found during the review of all supplied data.

About Thor

Thor Explorations Ltd. is a Canadian mineral exploration company engaged in the acquisition, exploration and development of mineral properties located in Nigeria, Senegal and Burkina Faso. Thor holds a 100% interest in the Segilola Gold Project located in Osun State of Nigeria and a 70% interest in the Douta Gold Project located in south-eastern Senegal. Thor also holds a 49% interest in the Bongui and Legue gold permits located in Houndé greenstone belt, south west Burkina Faso. Thor trades on the TSX Venture Exchange under the symbol “THX”.

THOR EXPLORATIONS LTD.

Segun Lawson

President & CEO